A real estate deal can involve millions of dollars. That’s why for many, syndication is the key to start investing in real estate. But, did you know that there’s actually a way for you to do a deal without using your own money? Our guest today, real estate entrepreneur Michael Gilman answered this question and more.

Our Gracious Sponsor

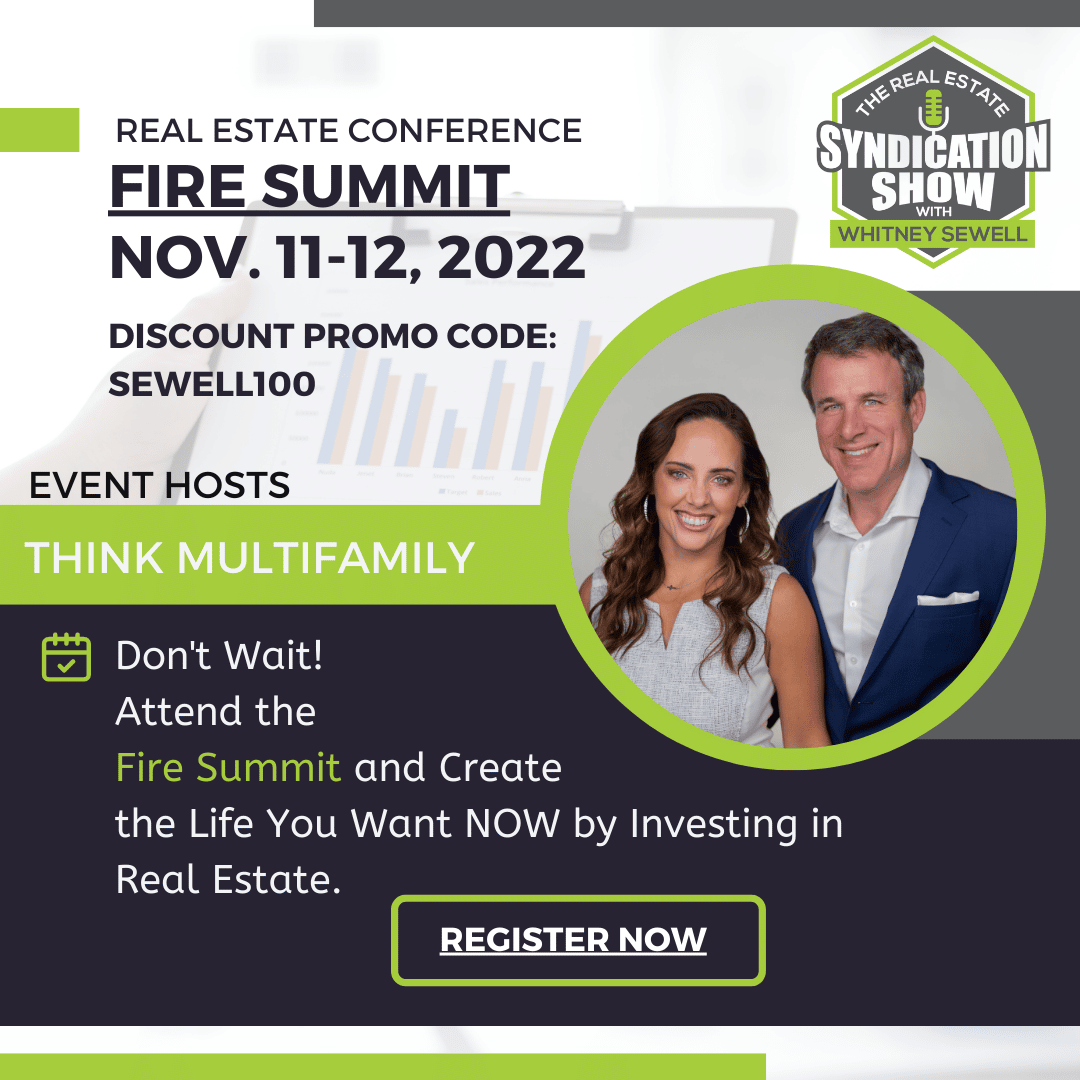

FIRE Summit 2022

Did you know that multifamily is one of the most recession-resistant strategies to create long-term equity and cash flow, and build wealth through real estate that can save you big on your taxes?

You don’t want to miss Think Multifamily’s annual Fire Summit conference on November 11th & 12th.

Go to thinkmultifamily.com/Fire for more information and to register today!

Enter Promo code: Whitney100 to save $100

![]()

Watch the episode here:

Listen to the podcast here:

Michael kicks off by sharing his background as a lawyer and how he transitioned to become a full-time real estate entrepreneur. He also talks about the reason why he chose to invest in real estate to grow wealth, how he derives his income from assets, and why he started buying cash flowing properties. He then discusses the pros and cons of having your own management company, why they chose to start their own management company from scratch, and ultimately, he gives tips on how to do a deal without using your own money. Listen now and enjoy the show!

Key Points From This Episode:

- Michael shares how he transitioned from being a lawyer to a full-time real estate entrepreneur.

- Where does Micahel currently invest in?

- Michael shares that in smaller markets, it’s hard to get larger deals.

- The pros and cons of having your own management company.

- Michael elaborates on ways you can start a deal without using your own money.

- Relationships are key in doing a deal without using your own money.

- Doing a deal without your own money is a high-risk strategy.

- How did Michael minimize the risks with this strategy?

- How does Michael raise capital now for bigger deals?

- Michael shares that when the pandemic hit, he saw it as an opportunity to pool capitals for his deals.

- Michael says changing focus to professional investors made a lot of difference for him and the way his business grew.

- Michael’s best source for meeting new investors right now.

- The most important metrics that Michael tracks.

- What are some habits that Michael is disciplined about that have produced the highest return for him?

- How does Michael like to give back?

Tweet This!

“What kind of really resonated or affected me was just how quickly things could evaporate.”

“[It] took me to real estate because it was tangible, it was real, and more specifically at time, just cash flowing.”

“I didn’t want to trade time for money forever. I wanted to build wealth, be an investor, and derive my income from assets. I started buying just cash-flowing real estate.”

“I think the easiest way, the most common way is first you need a cash flowing property, you need a property that the cash flow is going to be greater than your mortgage.”

“The first deal is always the hardest. So obviously, that’s the important step, kind of right sizing it for what you can raise.”

Links Mentioned:

Cross Mountain Capital website

About Michael Gilman

A former lawyer at Wall St. investment banks, Michael has been successfully acquiring and repositioning multifamily assets and generating exceptional returns on capital for over 10 years. After building his own real estate portfolio approaching 100 units across the northeast (self-managed through MSA Properties LLC), Michael established Cross Mountain Capital to bring best-in-class returns to sophisticated investors such as family offices, investment funds, and high-net-worth individuals looking to diversify their investment portfolios with real assets.

Before devoting himself full-time to Cross Mountain Capital, Michael was Head of Legal and Portfolio Management at Easyknock. He managed over $250+ million in residential properties and advised on legal matters related to the company and multi-state real estate business and legal issues.

Michael previously worked in legal and advisor capacities at Wall St investment banks Cantor Fitzgerald, Deutsche Bank, and Bank of America. He held Series 7, 24, and 57 licenses in the securities industry and is also a licensed real estate broker.

When he isn’t working, Michael is spending time with his family or pursuing one of his many hobbies related to the outdoors, including but not limited to skiing, trail running, mountaineering, and obstacle course races. Michael is a strong supporter of environmental causes and a member of POW (Protect Our Winters).

Michael holds a B.A. from Sarah Lawrence College and a J.D. from Brooklyn Law School.

Full Transcript

EPISODE 1475

[INTRODUCTION]

Michael Gilman (MG): I think the easiest way, the most common way is first you need a cash flowing property, you need a property that the cash flow is going to be greater than your mortgage.

Whitney Sewell (WS): This is your daily real estate syndication show. I’m your host Whitney Sewell. Today our guest is Mike Gilman, a former lawyer at Wall Street Investment Banks. Michael has over 10 years of experience acquiring and repositioning multifamily assets and generating exceptional returns on capital. After successfully building his real estate portfolio approaching 100 units across the Northeast, he self-managed self-managed through MSA Properties LLC. Mike established cross Mountain Capital to bring best in class returns to sophisticated investors such as family offices, investment funds, and professionals looking to diversify their investment portfolio into real estate. But before devoting himself full-time to cross Mountain Capital, Michael was head of legal and portfolio management at Easyknock. He managed over $250+ million in residential properties and advised on legal matters related to the company and multi-state real estate business and legal issues.

So a great background to have getting into real estate right? And Mike had just that he’s growing his company now it’s commercial real estate business. But he’s even we’ll talk a little bit about getting into how he got started into smaller real estate even without any of his own money and where that’s taken him now obviously, it’s grown a lot. He’s not still doing that. But he does share just a couple of tips around that. And he’s gonna dive into the current interest rate cycle good time to buy what you know, some things like that, that I know everybody is interested in at the moment.

[INTERVIEW]

WS: Mike, welcome to the show, honored to meet you and had you on. It’s interesting, you know, when I get to interview people and talk to folks who you know, spent a lot of time and energy building a career and having a career path that most would see crazy leaving and going and doing something as silly as real estate, right? It’s just grateful to have you on and I’m really encouraged by your story. I want the listeners to know more about you.

And so Mike, you know, who are you? Tell the listeners a little more about yourself, your background, let’s dive into that. To some degree. I know you’re a former lawyer on Wall Street. And, you know, that doesn’t happen just by thinking about, you know, kind of nonchalantly trying to get somewhere right, you know, no doubt that took a lot of time and energy. But let’s talk about that, you know, your background a little bit and how you got where you’re at now.

Michael Gilman (MG): Yeah, sure. You know, so I was always pretty entrepreneurial minded, kind of growing up, the only child my parents kind of were pushing me to be a lawyer, doctor, kind of listened to them and went to law school, became a lawyer, but was always again, I wanted to build wealth. And, I was always very much into economics, I was a big trader, I like trading, day trading, swing trading.

So I figured, well, let me just start here. Maybe I’ll transition over investment banking and trading. And so, anyway, that’s how I kind of I started on the legal side, this was in 2009, right in the middle of the great kind of housing bust and the meltdowns that we’re having on Wall Street. So it was pretty interesting time and you know, right away being there, at that time what, what kind of really resonated or affected me was just how quickly things could evaporate. Securities could evaporate all this wealth just overnight vanish and it’s something that affected me growing up.

And so kind of been there looking around you know, I was always searching for wealth. What’s the best way? Where should I put my money? And it took me, essentially, been on Wall Street, took me to real estate because it was tangible, it was real, and more specifically at time, just cash flowing. Real estate seemed like if you could buy a nice cash flowing property that was the cap rate was at a nice premium and a spread to your financing, it seemed tough to go wrong with that. It hung up just stabilized, you know, occupied property.

So with that in mind, and knowing that you know, I didn’t want to trade time for money forever, I wanted to build wealth, be an investor, and derive my income from asset. I started buying just cash flowing real estate. I was based in New York, and I found some really good deals in New England, they’re just not a lot investors up there. People are scared of the cold I think for one, you know, scared of the damage it does to the properties and snow. So you know, I found you could get 10 cappers plus with just heavy value-add. Value add and all kinds of ways because there was old mechanicals, so you could improve, lower your expenses, because heating was a big thing. Certainly it was all up. So just growth, pricing and efficiencies.

And then the big thing was, there was no supply and people build new developments up there. So you know, never had gangbusters growth. Actually, the lack of supply, in my opinion, made a much tighter rental market than many others. So it was like, in my view, just a great sleeper market. So I started like cobbling together, you know, multifamilies, but I’ll kind of stop there because I’ve said a lot.

WS: Yeah, no, it’s incredible. I appreciate your path, even where you’re investing a little bit because I was wanting to ask you what you’re currently investing in. What does that look like?

MG: Yeah, so you know, after a time doing that building, I kind of my own portfolio, it dawned on me to start pooling capital. And especially at this time I shifted my career more in real estate, I was at a startup. I was surprised at how easy it was to just to raise capital for startups that really easy just throw some projections on. I was just shocked, because this was a really risky stuff. And you know, most startups fail. So with the fact that there was so much capital available, it was like, “Well, you know, I have this, look at this little track record I’ve assembled, this is really safe stuff that is making great money.”

So I decided that point to pool capital. And that’s when we started focus, shifting strategies a bit. You know, one of the issues in New England, it’s a smaller market, it’s tough to get larger deals. And also, it’s not very liquid, you know, stuff could or traditionally it wasn’t very liquid. Now, it’s a different story. But, you know, stuff could linger on the market there. We wanted something where we could do a shorter hold, like a reposition in and out. And so we knew we had to be in a major market, went up more towards major markets to really pull capital, in my opinion, the way I wanted to. So that’s ultimately what took us to different markets.

I ended up after much kind of debate on where I wanted to plant my flag side on Colorado. And that was, for a number of reasons. One, one was obviously a great fundamentals, economics, population, very favorable business climate right there behind North Carolina, in many of the rankings. And then the big one, the second big one was it was a place, you know, I love to visit a lot of mountains. I’m a big skier, trail runner, and so it just resonated with me. So that’s where we started to focus expanding and kind of grew from there. One thing that was pretty important to us, or allowed us to succeed in New England was self management and construction. And that’s something we kind of replicated in Colorado, by partnering with already have already built kind of operation, existing construction property management company, where we’ve now essentially developed like exclusivity and really are scaling together with my partner, Phil over there.

WS: That’s interesting. That’s neat to know that because that’s constant conversation, it seems people having are wondering about is, you know, should I bring management or you know, construction in-house? Should I build those teams and try to do that myself or versus hiring a third-party and knowing that you can probably speak to some pros and cons of owning or having your own management construction companies?

MG: Yeah, absolutely. So you know, the stuff we’re doing Class C to B’s, maybe there’s some class B’s to B pluses, A minus. And those kind of repositions, they’re really hard to be honest with you, property management side is my least favorite side of the business. So it’s not something I kind of if I could have found a company that would have done it right, you know, repositioned it, how you know, kind of the key is just beat execution, coming in on budget on time. And it was just like, I couldn’t find an outfit like that.

And so that’s why we started doing it from scratch. And then, you know, going into Colorado, I didn’t want to do it from scratch, kind of did the next best thing which was integrate out that that was doing really well. But I mean, to me, it’s important because on these repositions, it’s being able to control your margins, your speed, you’re allocating crews, we we’ve gone through, we’ve had to fire a few property managers, coming to that conclusion,

WS: Yeah, it’s something I see a lot of operators go through, right, or numerous third party, or maybe they find a great one. Oftentimes, you hear nothing, but negatives, about third-party management. I mean, it’s something we’ve recently brought in house as well, it’s just done a number of things for us by doing that, but it’s a hard bandaid to pull off. And decided to do so but I know that you’re doing deals, you know without even using you know, some of your own money or your you know, develop methods of doing that.

Maybe speak to that a little bit. I know there’s people listening who would love to do that as well. Now, obviously, you know, we raise lots of money and do deals, we invest our own money, but we could do without our own money. But essentially, we’re still paying the team and doing all this stuff. But how do you see doing deals without using your own money?

MG: Yeah, and so I’ll speak to that in kind of smaller context. Certainly, when we pull capital, the one of the important things is for the sponsor to be in the stack and have skin in the game. So I’ll kind of talk about it outside of that when I was doing deals just just made or how anyone could really buy a property and not put in a single dollar. And so I think the easiest way, the most common way is first you need a cash flowing property, you need a property that the cash flow is going to be greater than your mortgage. It needs to be plus 1.25on the DSCR. So something so in my case, I was looking for stuff that was at least 300, 400-basis points spread to your cost of financing. So let’s say your debt is 6%.

You know, because if you’re using this strategy using high leverage, you really want a nice cushion. So I really want like a 400-basis points for at minimum I would say. And so you’re looking for 10 cappers out of the gate with value-add so back to have you not using your money.

So the typical commercial lender will come with 75%. So, you know, they’ll look at the property, cash flow, no problem on the underwriting though common 75% Most of them and these are especially like credit unions and regional banks, very relationship-based. And typically, if they trust in you, your business plan other 25% does not have to be your capital. So you get that from anywhere else, you get it from your friend, you borrow it from your friend, have them invest. Or in my case, what I was doing was I had a HELOC. So I was just pulling money from my HELOC to cover that capital contribution.

So that’s how I started building up cash flowing properties with kind of minimal upfront and the only way you know it’s a high risk strategy. So you need a really safe, cash flowing asset in my opinion.

WS: Yeah, that is a strategy I’ve heard different people use. And you talked about, you know, higher risk. And I would say yeah, one question, what happens if this property flip as a flop? And are you prepared for that? You know, the now that you’ve taken out the HELOC as well. What are some ways maybe you calculated that are thought through or even the risks of that?

However, I also say, before we get to that, you gotta be willing to take a few risks often to get started even or to make a big path or for investing and doing well in this business. But we’re our goal is to minimize all the risks possible. Right? And so how did you do that? Or how did you think through that with that type of plan?

MG: Yeah, absolutely. So you know, to me looking at it, there wasn’t much risk, at least compared to putting my money in the stock market, just because they this was a stabilized building that you could go back 10 years, it was like 100%, 95 to 100% occupied in a small town where there was no new development, like just things were steady, there was no volatility. So you know, it would really take some type of cataclysm, uninsurable event, in which case, I’d say, most people would be in trouble.

WS: Yeah, another reason we love real estate, right? I mean, you’re owning an asset, you have this physical thing. Hopefully, you’ve done your homework to know that it’s cash flowing, like you’re talking about, for sure. Speak to what does it mean when, because I just want to make sure everybody understands this, like you talked about, you know, the debt 6%. And you say you want at least a 400-basis point spread? What does that mean? Or maybe even walk us through that a little bit? So I can just ensure everybody understands what you’re talking about?

MG: Yeah, absolutely. So let’s say you’re borrowing a million dollars, right? And the coupon there is 6%. And let’s just make it simple. It’s interest only. Your annual interest payment for your cost of service, your debt is $60,000. So you want a property that’s going to cash flow in excess of that. So when I say a 10 cap, let’s just take that million dollars property for a million using 100% financing. That 10 cap, that means it should be thrown off, it would be thrown off about $100,000 here. So right there, you’re making $40,000, which is essentially that basis points.

WS: Okay. Now, it’s helpful. Now though, now that your business has grown now you’re, you’re raising money, you’re doing larger deals, speak to that a little bit, or moving into raising larger amounts of money now and go in that path versus sticking to that business plan, or maybe single-family or, you know, smaller residential.

MG: You know, after after doing this kind of strategy for quite some time. And I’m on stop, because I was on Wall Street. And I had like, I was up to like 60 units. And the last one was just a huge headache. And we were again, self managing, but it’s 60 units, like you’re self managing, there’s no outsourcing, right? So you’re dealing with everything.

And it was just anything that could go wrong will go wrong. It’s like a curse building. Like, mechanicals workers, just like everything, like a storm came by, the roof hatch blow off. And it was funny, because I went into it. And so here’s another one, we went into it, the ground floor was a commercial unit. And so we partnered with this local couple, they were farmers, and they had this great vision of this Organic Cafe. And that were, they’d sell this produce, and we kind of like, subsidized it, and so that they were just not very good at the business aspect of it. So they weren’t making any money. So you know, we spent just a lot of time with, like, this vision.

So anyway, I’m like, sitting here, I forget which bank I was, but there’s just, you know, 100 million dollar deals going off left and right. And I’m here dealing like I’m like, getting these emails about apartment issues. That’s $50,000. You know, that was the unit price that we were buying. It was $15,000 for last and I’m like, “What am I doing? You know, is this really like the right way?” And so I stop, stop for a bit, then COVID hit. And that’s, that’s really when rates went down. That’s where I saw the opportunity to pool capital and thought the time was right.

So yeah, I mean, essentially, it just got into larger buildings, because it was, in my opinion, if I was going to do a full-time and really make an income out of it and replace more than replace what I was making that this was the path to do that because I wasn’t really just gonna get there just aggregating little cash on properties. So that’s kind of what what sparked the transition.

WS: Yeah, no,that’s awesome, though. What about I just your growth in this in the commercial real estate business as well, or being able to raise enough money to do big deals and what were what were some of the steps you took to be able to get to where you’re at now?

MG: The first deal is always the hardest. So obviously, that’s the important step kind of right sizing it for what you can raise. Our first deal it was we raised to 2.6 million. It was tough on hindsight, you know, we probably should have started smaller. And that was friends and family at first, like your first deal. Most people, it’s likely going to be friends and family. So that’s the tough part. Also, because they know you for like me, I was like we are trained attorney like, what are you doing? And so just doing that mindshift, change is tough.

And, but eventually, at least for me, it was clear that to really scale, kind of the focus, I changed my focus to professional investors. And for me, I don’t like raising capital, I don’t like you know, it’s tough to aggregate, you know, large sizes with individual check writers. So that’s kind of what led us to transition more to institutional check writers. You know, it sounds great.

Everyone’s like, “Yeah, please, I’d love you know, one large check.” But you have to also realize your economics can get really squeezed they’re like kind of the the waterfalls you could pass off and, you know, retail or individual syndications, you just get eviscerated with larger investors.

WS: Capital is a lot more expensive that way, isn’t it? You know, Mike, what about everybody has the question right about where we’re at in this interest rate cycle or, or just the economy in general? Or is it a good time to buy or not? What are your thoughts and how your business is moving forward right now?

MG: Yeah, so I’d personally since 2009, when they started easing and flooding the system with liquidity, I thought that higher rates would would end inflation would follow quite shortly thereafter. And so I was just perpetually stunned and taken aback when it never materialized, and the fact the easing kept coming, and the the fact that it’s finally happening, and it’s finally here, it’s really just interesting because I almost got into this mindset that the can could be kicked perpetually.

You know, the kind of the rate at which it’s happening, I think, is much, certainly steeper and faster than anyone predicted. I think it’s destabilizing and they’re probably overdoing it. And I think it’s gonna, we’re bearish. I think it’s gonna cause liquidity issues going into 2013. If they keep this up, I think there’s going to be continued price softening and look for real estate for all assets. And so, we were bearish during such times.

I think there’s opportunities because when the dislocations happen, that’s when people tend to need to sell at depressed prices. And we’re just looking at some stats, there’s like, and then there’s just one stat, about $50 billion of bridge loans that were taken out that are coming due next year, for which the DSCR ratio is just unsupportable. They can’t get refinance, like this stuff has to hit the market. And some people say that’s just the surface. So I definitely think there’ll be pricing pressure.

And so we’re, we’re buyers at the right price. And especially with the right financing structure, certainly debt assumptions look really good seller financing, anything like that, we started doing foot taking full recourse bank loans, just because the spreads are tighter there. So yeah, kind of how we’re approaching it.

WS: What’s your best source for meeting new investors right now?

MG: So honestly, it’s I’m just having a deal like myself, I’m not very social, I don’t want to like go into like conferences. I’m just not, I’ve never been one to really put myself out there. So we we tend to do is we get a deal. And we’ll go to market with it. We have some good broker relationships that will always introduce us to new investors. So, with each new deal, we always try to get it in front of new people because then they look at it, they ask questions like most of them, like whatever eight out of 10 will pass, but you added them to your Rolodex and the next time they’re familiar with you, they know you, they’ve seen your deals before and it just becomes easier and your network kind of just expands.

That’s how we have been pretty successful at building out our network is just by having like good deal flow, which another aspect we haven’t spoken about was, you know, when we pivoted markets, one of the things we focused on was off-market acquisitions and building out but we partnered with a company offered who’s become a great partner for us to source off-market. And that was pretty big for us just having, you know, really appetizing deals.

WS: That’s helpful and thinking through that or how you all finding or how you’re working through value investors, even though it’s not going to networking events and things like that it can still be done. Right? What about what are some of the most important metrics that that you track? It could be personally, professionally. I just wonder, like, what’s important to people, you know, they thinking through, it could be your your bench press, or you know, or it could be you know, I want to know this about, you know, I want to make sure we’re underwriting this many deals, but what are what are some of those things for you?

MG: Yeah, it’s really the asset management, the deal execution and making sure we’re, you know, we always like to underwrite the deal so that we can exceed our pro forma. So doing variance reports, just on the asset management, drilling down into where we are with expenses, where we are with capex budgets, had the unit turns and vacancies, especially on the heavier value added lifts like we you know, we have buildings we’ve taken over that were Are 50% occupied. And so get getting those up and fully rented is not that easy. Because it’s when you have something that’s vacant, it’s just harder to lease it like it’s less appealing, right? So just being on top of all these metrics that leads to our us coming in ahead of our projections is really what we focus on the most, for sure.

WS: What are some habits that you are disciplined about that have produced the highest return for you?

MG: Yeah, I’d say making sure you get enough rest and exercise, just very simple things like that. I mean, for me, a big part of is, you know, I’m big into exercising, like I love running, for example, on the trails, I clears my head, like solve problems, you get into like these flow states, and just combine that with being well rested and not stressed, has kind of been key to just managing huge kind of multitasking and moving the ball forward and when you have all these things going on as a sponsor.

WS: It’s interesting, I hear numerous people talk about just exercise and what that does for them in so many different ways. And I’ve still gotta get my tail kicked in gear to get back to exercising. What about, how do you like to give back?

MG: Yeah, so um, you know, the certainly a big part for us. We donate to a number of nonprofits on environmental causes, protect our winters, wild bird society. You know, my parents are actually from another country that from the Ukraine, first generation born here, but kind of what’s going on there is is just shocking, horrifying, and donating some of our profits and sending that way and working with or we can outsourcing to some third-party Ukrainian firms.

WS: Mike, it’s been a pleasure to meet you and have you on the show. And I look forward to staying connected with you. And on that note, how can the listeners connect with you as well and learn more about you?

MG: Yeah, so I’m active on social media. It would be LinkedIn. Mike Gilman is my handle there, check out our website, crossmountaincapital.com. Or you could sign up for our distribution list or just reaching out to me directly — mike@crossmountaincapital.com.

[END OF INTERVIEW]

[OUTRO]

WS: Thank you for being a loyal listener of the Real Estate Syndication Show. Please subscribe and like the show. Share with your friends so we can help them as well. Don’t forget, go to LifeBridgeCapital.com where you can sign up and start investing in real estate today. Have a blessed day!

[END]

Love the show? Subscribe, rate, review, and share!

Join the Real Estate Syndication Show Community:

")